In late 2019, the Internal Revenue Service (IRS) and Treasury Department issued a final answer to the question of whether large gifts made between December 31, 2017, and January 1, 2026, would adversely affect post-2025 estates. The regulation confirms that individuals who want to take advantage of Tax Reform’s gift and estate tax exclusions can do so without the concern over losing the tax benefit of the higher, albeit temporary, exclusion level.

Background

The Tax Cuts and Jobs Act (TJCA) doubles the basic exclusion amount (BEA) from $5 million to $10 million (before inflation adjustments). However, this increase is temporary, with exclusion amounts set to return to pre-2018 levels on January 1, 2026. In combination with the flat 40% estate tax, the regulation was received with excitement. Still, it quickly turned to concern as taxpayers contemplated what would happen to their tax benefits should they die after December 31, 2025.

The Solution

The final regulations provide a special rule that allows the estate to compute its estate tax credit using the higher exemption amount applicable to gifts made during life or the amount applicable on the date of death.

Taxpayers should note that if their gift amounts fall below the 2026 amount, their exemption will be based on the exemption amount at death. If you are considering a large gift or have clients who are unaware of these changes, it is important to understand this tax credit is a limited time offer. The regulations only apply to qualifying gifts made between 2018-2025. Contact the professionals in our office if you have questions about how these changes will affect you or your organization.

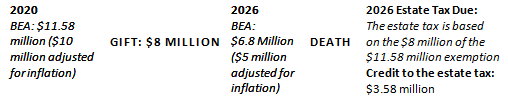

Formula Logic:

Under the new regulations, the credit applied to compute the estate tax is based on the (theoretical) $8 million of the $11.58 million exemption ($10M adjusted for inflation) used to compute the gift tax credit. In other words, the estate won’t have to pay tax on the $1.2 million in gifts that exceeds the exemption amount at death ($8 million less $6.8 million), and the credit to the estate tax will reflect the $3.8 million of the amount remaining after the gifts were made ($11.58 million less $8 million).

Source: https://gbq.com/irs-confirms-large-gifts-now-wont-hurt-post-2025-estates/